Climate-Resilient Home Insurance for Coastal Properties: A Strategic Framework for the Future

Introduction: The New Reality of Coastal Living

Coastal living has long been the pinnacle of residential luxury and lifestyle. However, as the global climate undergoes unprecedented shifts, the idyllic shorelines of the world are becoming frontiers of significant financial and physical risk. For homeowners, the primary concern is no longer just the aesthetic appeal of a property, but its survival in the face of rising sea levels, intensifying cyclonic activities, and perennial erosion. In this context, the insurance industry is undergoing a radical transformation. Traditional home insurance is proving inadequate, giving way to a more sophisticated, climate-resilient framework designed to mitigate the specific perils of coastal geography.

Climate-resilient home insurance is not merely a financial safety net; it is an integrated strategy that combines risk transfer with proactive adaptation. As insurance premiums in high-risk zones continue to soar, understanding the mechanics of these new policies is essential for property owners, investors, and developers alike.

The Physics of Peril: Why Coastal Insurance is Changing

The fundamental premise of insurance is the predictability of risk. Historically, insurers used actuarial data based on the past 50 to 100 years to determine premiums. However, climate change has rendered historical data less reliable. Coastal properties are now facing ‘compound events’—where high tides, storm surges, and heavy rainfall occur simultaneously, overwhelming traditional drainage and defense systems.

Global sea levels are projected to rise significantly by the end of the century, putting trillions of dollars in real estate at risk. Consequently, the insurance market is shifting from a model of ‘indemnity’ (compensating for loss) to ‘resilience’ (incentivizing the reduction of loss). This shift is necessary to ensure the long-term viability of coastal real estate markets.

Defining Climate-Resilient Insurance Features

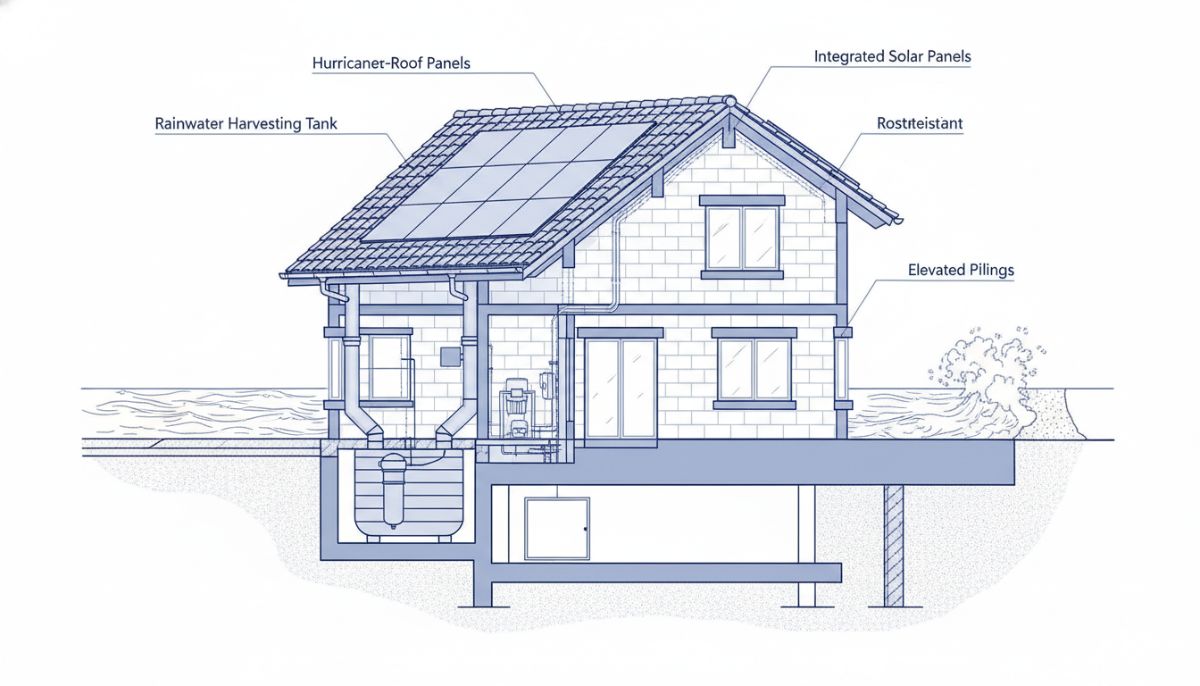

A climate-resilient insurance policy differs from standard homeowners’ insurance in several key ways. First, it often includes specific provisions for ‘Resilient Rebuilding.’ Traditional policies typically pay to restore a home to its pre-loss condition. Resilient policies, however, provide additional funding to upgrade the home to higher standards of durability—such as installing impact-resistant windows, elevating electrical systems, or using flood-hardened materials.

Secondly, these policies are increasingly linked to community-level defenses. If a coastal municipality invests in mangrove restoration or artificial reefs to break wave energy, insurers may offer lower premiums to the residents of that area. This creates a symbiotic relationship between private property protection and public infrastructure.

The Rise of Parametric Insurance Models

One of the most innovative developments in coastal protection is parametric insurance. Unlike traditional insurance, which requires a lengthy claims adjustment process to determine the actual value of damage, parametric insurance pays out a predetermined amount based on the occurrence of a specific event.

For example, a policy might trigger an automatic payment if a Category 3 hurricane passes within 50 miles of the property, or if the water level reaches a certain height. This provides homeowners with immediate liquidity to begin emergency repairs or evacuation, preventing secondary damage like mold growth or structural collapse that often occurs while waiting for a traditional adjuster.

Mitigation as a Driver of Affordability

For many coastal homeowners, the primary challenge is the affordability of premiums. Insurers are now providing clear roadmaps for premium reduction through mitigation. These strategies are often categorized into ‘hard’ and ‘soft’ measures.

Hard Mitigation Measures

1. Elevation: Raising the primary living areas above the Base Flood Elevation (BFE).

2. Structural Fortification: Using hurricane straps, reinforced garage doors, and impact-rated glazing.

3. Flood Vents: Allowing water to flow through non-living spaces (like crawlspaces) to equalize pressure and prevent foundation failure.

Soft Mitigation Measures

1. Nature-Based Solutions: Maintaining coastal dunes and native vegetation that act as natural buffers.

2. Sustainable Drainage: Utilizing permeable pavers to reduce runoff and localized flooding.

By documenting these improvements, homeowners can move their properties into lower-risk tiers, significantly reducing the annual cost of coverage.

Technology and Predictive Analytics

The future of coastal insurance is driven by Big Data. Insurers are now using satellite imagery, IoT (Internet of Things) sensors, and AI-driven flood modeling to assess risk at the individual property level rather than by zip code. This granularity allows for more fair and accurate pricing.

A homeowner who has invested in a private sea wall or specialized flood barriers can now prove their reduced risk profile through real-time data, ensuring they are not penalized by the general vulnerability of their neighborhood. This data-centric approach also helps buyers perform better due diligence before purchasing coastal assets.

The Role of Government and the National Flood Insurance Program (NFIP)

In many regions, the private insurance market is supplemented by government-backed programs. In the United States, the NFIP’s ‘Risk Rating 2.0’ is a prime example of the shift toward actuarial transparency. It aligns premiums more closely with actual flood risk. However, as government subsidies are phased out to reflect true costs, the importance of private-sector climate-resilient products becomes even more pronounced. A hybrid approach—where government covers catastrophic tail-risk and private insurers handle specialized resilience—is becoming the global standard.

Conclusion: A Proactive Approach to Coastal Investment

The era of ‘set it and forget it’ insurance is over for coastal properties. Climate-resilient home insurance represents a necessary evolution in how we value and protect our most vulnerable real estate. For homeowners, the message is clear: resilience is no longer optional.

Investing in a property that is built to withstand the elements, and securing insurance that rewards that foresight, is the only way to maintain the long-term value and safety of coastal assets. As we move forward, the collaboration between insurers, engineers, and homeowners will be the defining factor in whether our coastlines remain habitable or become relics of a more stable climatic past. By embracing these resilient frameworks today, we ensure that the beauty of the coast can be enjoyed by generations to come.